To prepare yourself and your finances for the 2021/22 tax year, here’s a selection of tax planning opportunities for you to explore.

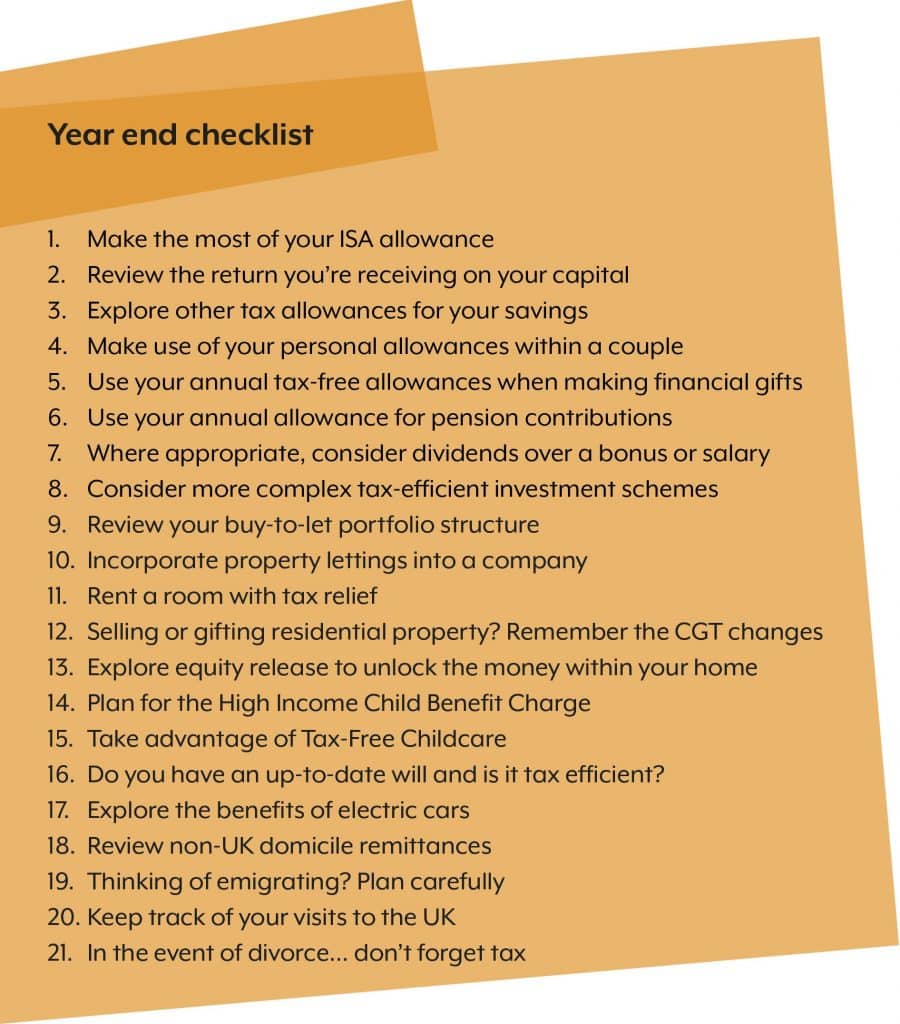

Make the most of your ISA allowance

ISAs are free from income tax and capital gains tax (CGT). The overall ISA allowance is currently £20,000 – this doesn’t carry over between tax years, so it makes sense to use as much of your allowance as you can afford to by 5 April each year.

The limits for different ISA types are:

| ISA | 2020/21 limit |

| Cash, Stocks and Shares, Innovative Finance ISA | £20,000 a year |

| Junior ISA | £9,000 a year |

| Help to Buy ISA | £200 a month for existing accounts |

| Lifetime ISA | £4,000 a year with no monthly maximum amount |

Review the return you’re receiving on your capital

Whether you have funds on deposit receiving a low return, or you rent property and are affected by the reduction in tax relief on loan interest, the return on capital or annual yields should be reviewed.

Our tax experts would be happy to advise on tax aspects that may be affecting you, whilst our team at BKL Wealth Management can review and advise on your personal or family wealth and assets.

Explore other tax allowances for your savings

For savings held outside pensions and ISAs, the government gives several other allowances. These include the Personal Savings Allowance: a tax-free allowance for interest payments. It is £1,000 for basic-rate taxpayers and £500 for higher-rate taxpayers but doesn’t apply to additional-rate taxpayers. All taxpayers also receive a £2,000 tax-free allowance for dividend income.

It is worth speaking to us to explore whether you are making best use of these allowances.

Make use of your personal allowances within a couple

If you are married or in a civil partnership, you may be able to save money by structuring your finances as a couple to ensure you are using both spouses’ tax allowances. This could be an especially good idea if one spouse pays tax at a lower rate than the other.

Use your annual tax-free allowances when making financial gifts

Each tax year you can make a range of tax-free financial gifts. These leave your estate immediately and won’t be taken into account when calculating your inheritance tax (IHT) bill.

These gifts could include: gifts to your husband, wife or civil partner (as long as the UK is their permanent home); unlimited individual gifts of up to £250 per person; unlimited payments towards the living costs of a child, elderly dependant or ex-spouse.

Do you know the value of your estate and have you considered IHT planning? We would be happy to have an initial conversation with you. We have more information here.

Use your annual allowance for pension contributions

Investments in your pension are free from income tax and CGT. Because of these and other tax benefits, there is a limit to the amount you can pay into your pension. Each year you can contribute as much money as you earn, usually up to £40,000 (although this tapers down to £4,000 for higher earners). You may also be able to make extra contributions by carrying forward any unused allowance from the last three tax years.

Basic rate tax relief is obtained at source and higher rate tax relief is obtained via your annual tax returns. In the right circumstances the net cost of making a contribution can be very low!

In addition to maximising the tax relief on pension contributions, our team at BKL Wealth Management would be happy to review your current mortgage arrangements. In general, pension schemes have become more efficient over time and therefore if you do have an older policy we would always recommend a review.

Where appropriate, consider dividends over a bonus or salary

A bonus or salary is generally tax deductible for the company, with up to 25.8% in combined employer and employee national insurance contributions (NICs). Dividends are free of NICs when paid. The Dividend Allowance charges £2,000 of the dividend income at 0% tax.

Consider more complex tax-efficient investment schemes

If you are a higher-rate or additional-rate taxpayer who can tolerate a high level of investment risk, you could also consider more complex tax-efficient investments such as Venture Capital Trusts, the Enterprise Investment Scheme (EIS) or the Seed Enterprise Investment Scheme (SEIS). These offer generous tax breaks (income tax and CGT) to offset the added risks of investing in smaller, younger and unquoted companies.

We have more information EIS and SEIS here.

Review your buy-to-let portfolio structure

If your spouse or civil partner is a basic rate taxpayer while you are a higher rate taxpayer, or vice versa, it makes sense for the lower earner to be the one who receives taxable rents from any buy-to-let properties you own. In certain circumstances it is possible to split income to an unequal share.

A review of any borrowings on your main residence and investment property would also be worthwhile.

Incorporate property lettings into a company

To handle the running of a property letting business, the formation of a limited company may have tax advantages.

Rent a room with tax relief

Under the government’s Rent a Room Scheme, you can earn up to £7,500 per year tax-free from letting out furnished accommodation in your main residence. That is halved if you share the income with your partner or another person.

Selling or gifting residential property? Remember the CGT changes

On 6 April 2020, capital gains tax (CGT) on property changed. This is likely to have a significant effect on the amount of tax you hand over to HMRC following a property disposal. So if you are thinking of selling or gifting a property, we recommend you plan accordingly. Please contact us for more details or read our article here.

Explore equity release to unlock the money within your home

If you’re a homeowner who’s retired or near retirement, equity release is a way of using the value of your property towards your financial needs and goals, from paying off debt or supplementing income to booking a dream holiday or helping younger family members onto the property ladder.

Our team at BKL Wealth Management can advise you on the pros, the cons and the options in the expanding equity release market.

Plan for the High Income Child Benefit Charge

Under this tax charge, the government recovers some or all of any Child Benefit claimed where the annual taxable income of the claimant or of the claimant’s “partner” (i.e. spouse, civil partner or cohabitee) exceeds £50,000.

To keep your taxable income below that threshold, you could reduce it by exchanging salary in return for employer pension contributions, or by making personal pension contributions.

Read our article on Child Benefit pension benefits here.

Take advantage of Tax-Free Childcare

The Tax-Free Childcare scheme could enable you to receive up to £2,000 a year for each of your children to help with childcare costs. For every £8 you pay your childcare provider, the government will pay £2.

Do you have an up-to-date will and is it tax efficient?

It’s a basic point that is commonly overlooked. A will may have been made pre or post-marriage but not updated following the birth of children.

Explore the benefits of electric cars

If you’re considering an electric or low emission vehicle for business use, the tax-related advantages are also worth exploring. They cover capital allowances, car benefits in kind (determined by the level of a car’s CO2 emissions and its fuel type) and fuel benefits in kind.

Our article here has more about the tax advantages of electric and low emission vehicles.

Review non-UK domicile remittances

If you’re not domiciled in the UK and you have an offshore fund in which “clean capital” is mixed with foreign income, foreign gains or both, you can arrange the income, gains and capital into separate accounts in order to facilitate tax-efficient remittances to the UK.

Reviewing your remittances before 5 April each year is important.

Find out about our complete UK tax service to non-resident and non-domiciled individuals here.

Thinking of emigrating? Plan carefully

Broadly, non-UK residents do not pay UK tax on their foreign income. But to understand in detail how permanently leaving the UK would affect your tax situation, forward planning with specialist guidance is essential.

Read our recent article on tax issues when leaving the UK here.

Keep track of your visits to the UK

Your residence status depends on how many days you spend in the UK in the tax year. This in turn affects your UK tax liabilities.

In the event of divorce… don’t forget tax

The principal CGT benefit of marriage – namely the ability to transfer assets between spouses on a no-gain, no-loss basis – lasts only until the end of the tax year in which spouses separate if the separation is by deed, court order or otherwise likely to be permanent. So if you and your spouse are having differences, your accountant’s advice (should you think to ask them) is likely to be to stick it out until 6 April if you possibly can.

If on the date on which the no-gain no-loss treatment is lost (which will always be 5 April), spouses remain married, they will remain “connected persons” for CGT purposes until decree absolute. This interim period delivers the worst of both worlds in CGT terms. Any transfer of assets during this period is deemed to be made at market value, with CGT payable accordingly, but if the transfer results in a loss for CGT purposes, the loss is “clogged”. This means that it is not available against gains generally but can be used only against gains on any other disposals made to the spouse before the marriage ends. That, in practice, often makes the loss useless.

All of this applies equally for marriage and for civil partnership. It does not, however, apply to unmarried (or un-civil-partnered) cohabitees: “common law” marriage has no significance for the tax purposes mentioned above.

Find out more in our article on tax and divorce here.

Finally, a bonus tip:

Speak to specialists for help with tax

Our tax and wealth management specialists are experienced at helping clients make the most of tax rules and allowances, structuring their finances tax-efficiently to ensure they don’t pay more tax than is necessary.

As well as advising you directly, we can arrange an initial consultation with one of BKL Wealth Management’s financial planners. There is no cost for this consultation – it is an opportunity for you to discuss your specific circumstances and goals with an experienced financial planner. If you choose to take up any of their services, all costs will be agreed in advance.

For more information, please get in touch with you usual BKL contact or use our enquiry form.

Our webinar, recorded earlier this year, will also take you through our year end tax planning tips: