Updated: 18 August 2022

One of the most generous tax reliefs available to companies is relief for research and development (R&D). If your company qualifies under the scheme for small or medium sized enterprises, it can claim an additional tax deduction of 130% of its qualifying R&D expenditure, meaning that it would get £230 of tax relief for every £100 spent.

Loss-making companies can benefit too, surrendering their R&D related losses for a tax credit at 14.5% and having up to 33.35% of their R&D expenditure subsidised by government funds.

In this article, we’ll report on a change to R&D tax credits from April next year and explore how HMRC’s latest statistics shed light on the take-up of R&D tax credits.

R&D tax credits statistics

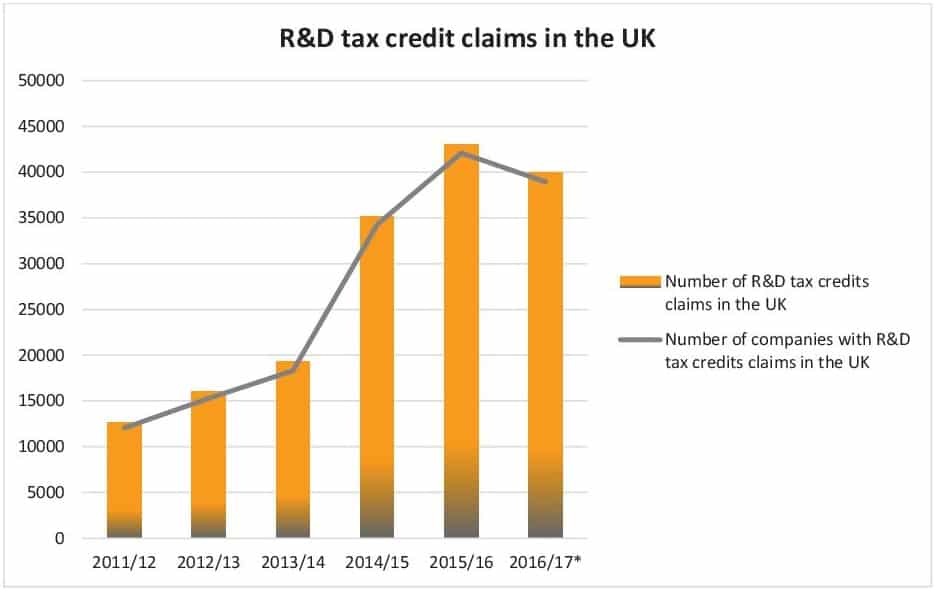

The number of R&D tax credit claims and the companies with those claims in the UK have both been increasing since 2011:

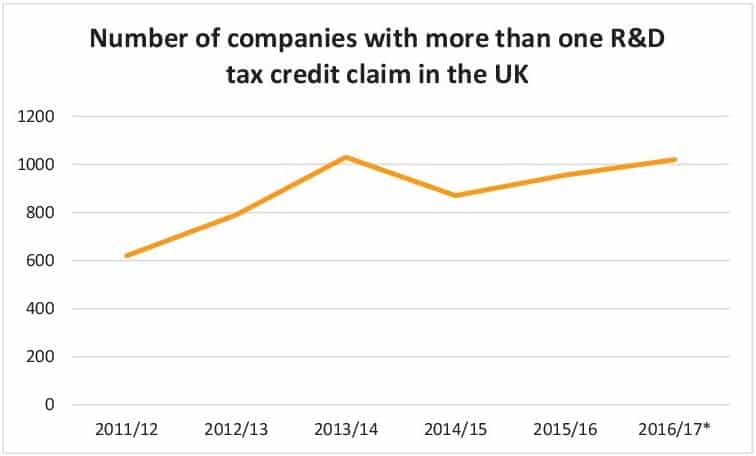

In the 2016/17 financial year, there were more companies with multiple claims than in 2011/12, but not through a steady increase. In 2014/15 there was a decline:

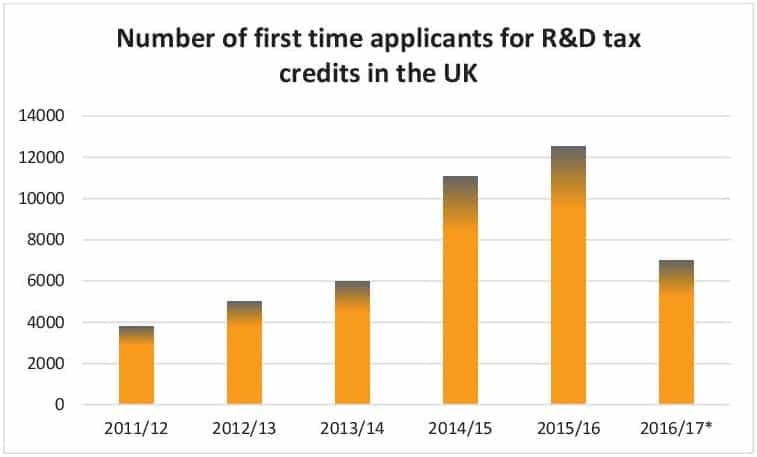

The number of first time applicants for R&D tax credits in the UK has seen increases over the past decade. Between 2011/12 and 2014/15, it more than tripled:

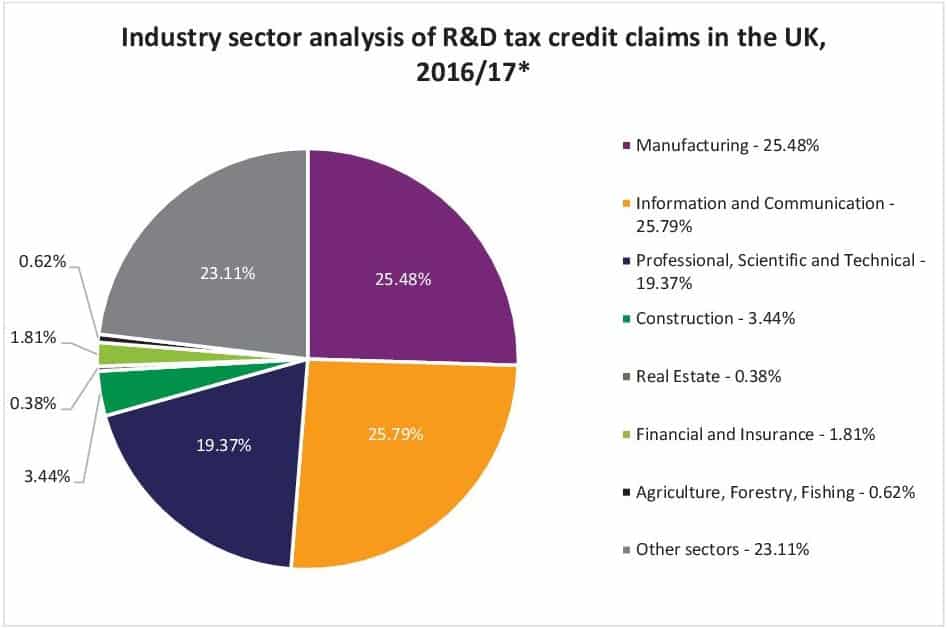

The sectors with the most R&D tax credit claims in 2016/17 were Manufacturing and Information & Communication, followed by Professional, Scientific & Technical.

Construction, Real Estate, Financial and Insurance, and Agriculture, Forestry, Fishing each account for a very small percentage of claims in the UK:

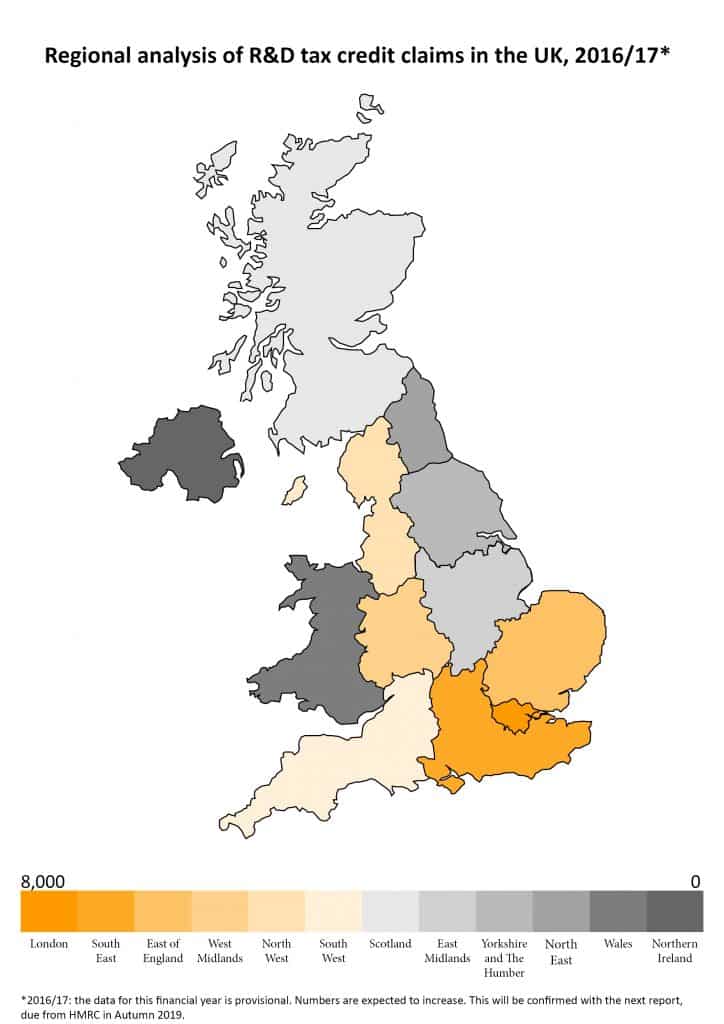

A regional analysis of the UK’s R&D tax credit claims in the UK during 2016/17 shows that London, the South East, and East of England made the most claims. The three regions with the least claims were the North East, Wales and Northern Ireland:

This information is also available in a pdf which you can download here.

All data is based on the HMRC’s Research and Development Tax Credits Statistics report (September 2018), available here.

*2016/17: the data for this financial year is provisional. Numbers are expected to increase. However, this will be confirmed with the next report, due in Autumn 2019.

Restriction of R&D tax credits, planned changes

Updated: 18 August 2022

Whilst the government is keen to encourage investment in R&D activities, it is concerned that the generous relief is being abused. Having estimated that £300m of credits have been paid in error, the government put a cap on the tax credit payable. The cap, which came into force in April 2021, will be £20,000 plus three times the company’s total PAYE and NIC liability for the year of the R&D claim.

If your company is claiming R&D relief for work largely carried out by UK employees, this restriction should have no impact on you. It is targeted at companies which, in fraudulently claiming the relief despite having no real presence in the UK, are making no contribution to the UK economy. HMRC estimated that the restriction would only affect 5% of companies currently claiming tax credits.

However, it restricts the tax credit available if your company doesn’t have many employees and instead uses subcontractors to perform R&D activities. Such companies may well be genuinely involved in R&D activities in the UK but have opted not to employ individuals for commercial reasons. In these cases, the cap will still apply and the tax credit available will be reduced, potentially to nil, but any losses which cannot be surrendered for a tax credit because of the cap will be carried forward for use against future profits under the normal loss relief rules.

In July 2022, the government released draft legislation which confirms the proposed changes to R&D claims for accounting periods starting on or after 1 April 2023.

In summary:

- No relief will normally be available for R&D undertaken by subcontractors or externally provided workers based outside the UK.

- All claims will have to be submitted digitally. There will also be a requirement to provide a breakdown of costs and supporting narrative.

- Companies will have to inform HMRC within six months of the end of an accounting period that they intend to make a claim. However, this will not be necessary where a claim has been submitted in respect of any of the previous three chargeable accounting periods.

- The reliefs are to be extended to include costs of datasets and cloud computing.

How we can help

BKL’s tax specialists have generated significant tax refunds and savings for clients investing in R&D. The projects have ranged from fingerprint recognition systems to robotic machinery for the flat-glass industry. Many of the clients we’ve assisted have undertaken groundbreaking software work.

There are pitfalls in the legislation and there are time limits for making claims. But by addressing these issues early, we have succeeded in obtaining HMRC’s agreement to the vast majority of claims submitted.

To find out more, get in touch today.